U.S. Census

Total Construction

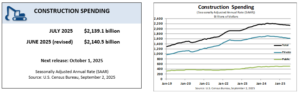

Construction spending during July 2025 was estimated at a seasonally adjusted annual rate of $2,139.1 billion, 0.1 percent (±0.8 percent)* below the revised June estimate of $2,140.5 billion. The July figure is 2.8 percent (±1.5 percent) below the July 2024 estimate of $2,200.7 billion. During the first seven months of this year, construction spending amounted to $1,232.7 billion, 2.2 percent (±1.0 percent) below the $1,259.9 billion for the same period in 2024.

Private Construction

Spending on private construction was at a seasonally adjusted annual rate of $1,623.3 billion, 0.2 percent (±0.5 percent)* below the revised June estimate of $1,626.3 billion. Residential construction was at a seasonally adjusted annual rate of $886.5 billion in July, 0.1 percent (±1.3 percent)* above the revised June estimate of $885.9 billion. Nonresidential construction was at a seasonally adjusted annual rate of $736.7 billion in July, 0.5 percent (±0.5 percent)* below the revised June estimate of $740.4 billion.

Public Construction

In July, the estimated seasonally adjusted annual rate of public construction spending was $515.8 billion, 0.3 percent (±1.6 percent)* above the revised June estimate of $514.3 billion. Educational construction was at a seasonally adjusted annual rate of $111.7 billion, 0.1 percent (±1.8 percent)* below the revised June estimate of $111.8 billion. Highway construction was at a seasonally adjusted annual rate of $142.8 billion, 0.1 percent (±4.8 percent)* below the revised June estimate of $142.9 billion.

AGC:

Construction Employment Dips in August

Construction sector employment declined by 7,000 positions in August and has remained little changed since December, according to an analysis of new government data by the Associated General Contractors of America. Association officials noted the results are consistent with a survey the association released last week that found many owners have canceled, deferred or scaled back projects due to tariffs and labor shortages.

“The latest figures show that nonresidential construction—not only homebuilding—has stalled,” says Ken Simonson, the association’s chief economist. “That fits with reports that owners have hit the pause button on many projects, in large part because of uncertainty over the impact of tariffs and other policy upheavals, as our workforce survey found.”

More information

Despite the lack of employment growth, the unemployment rate for recent construction industry workers in August was 3.2%, tying the record low for August set in 2024, Simonson noted. He said the low industry rate likely is a result of workers leaving the industry to avoid being swept up in immigration enforcement actions, as the association’s survey also indicated.

Construction employment in August totaled 8,295,000, seasonally adjusted, a decline of 7,000 from July and the third consecutive monthly decrease of 13,000 from July. Industry employment has risen by a net of only 6,000 or less than 1% since December.

In August, nonresidential construction firms shed a net 1,200 employees, as losses of 3,300 at nonresidential building construction firms and 200 among specialty trade contractors offset a gain of 2,300 workers at heavy and civil engineering firms. Residential construction employment declined by 6,100, including 900 jobs at homebuilders and other residential building construction firms and 5,200 at specialty trade contractors.

The 2025 AGC of America-NCCER Workforce Survey found that 16% of construction firms reported owners had canceled, postponed, or scaled back projects resulting from changes in demand or need due to tariffs. Roughly one-fourth, 26%, of contractors experienced project setbacks resulting from changes in demand or need due to policy changes in areas such as federal funding, taxes, or regulations. In addition, 28% of firms reported immigration enforcement actions in the past six months had affected their projects.

Association officials said these policy upheavals affecting costs, funding, and employment were delaying vitally needed infrastructure, job-creating manufacturing projects, and much-needed housing. They urged officials in Washington to stabilize trade policy and to better target immigration enforcement in a way that does not disrupt construction

“The economy depends on construction,” says Jeffrey D. Shoaf, the association’s chief executive officer. “Constant changes in tariffs and other federal policies, and misdirected immigration enforcement are interfering with the industry and the broader economy.”

ABC: Construction Materials Prices Up 0.2% in August, Driven By Iron and Steel |

|

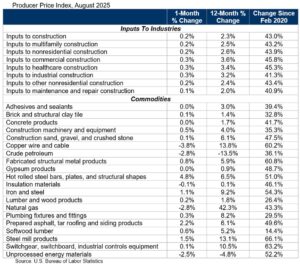

| Construction input prices increased 0.2% in August compared to the previous month, according to an Associated Builders and Contractors analysis of the U.S. Bureau of Labor Statistics’ Producer Price Index data released today. Nonresidential construction input prices also increased 0.2% for the month.

Overall construction input prices are 2.3% higher than a year ago, while nonresidential construction input prices are 2.6% higher. Prices decreased in all three energy categories last month. Crude petroleum and natural gas prices were both down 2.8%, while unprocessed energy materials prices decreased 2.5% in August. “Construction materials prices rose modestly in August, although the increase would have been larger if not for declining oil and natural gas prices,” said ABC Chief Economist Anirban Basu. “Prices rose at an especially rapid pace in some of the categories most affected by tariffs. Iron and steel prices, for instance, are now up 9.2% on a year-over-year basis, while copper wire and cable prices are up 13.8%. Even though nonresidential input prices have risen at a 5.3% annualized rate in 2025, contractors remain broadly optimistic about their profit margins over the next six months, according to ABC’s Construction Confidence Index.” |

AIA -

No turnaround in sight for spending on nonresidential buildings

There is some good news and some bad news in the latest outlook for nonresidential construction spending on buildings, according to the latest AIA Consensus Construction Forecast. First the good news: In spite of stubbornly high long-term interest rates, inflation rates stalled above the Federal Reserve Board’s target, falling consumer confidence scores, disappointing levels of home building activity, rising tariff rates for many inputs to construction, and construction labor shortages exacerbated by restrictive immigration policies, the outlook for the remainder of the year and into 2026 is largely unchanged from where it was at in the beginning of the year.

The bad news: The outlook for spending entering the year was very pessimistic.

The consensus is that overall spending on nonresidential buildings not adjusted for inflation will increase only 1.7% this year and grow very modestly to just 2.0% next year. The commercial sector outlook is about on par with the broader industry, with a projected 1.5% increase this year rising to 3.9% in 2026. Spending on the construction of manufacturing facilities—the industry bright spot in recent years—is expected to decline 2.0% this year, with an additional decline of 2.6% next year. Institutional facilities are expected to be the strongest sector with projected gains of 6.1% this year and another 3.8% in 2026.

View interactive data from the Consensus Construction Forecast